Offers

Offers Rates

Rates Debit Card Related

Debit Card Related Credit Card Related

Credit Card Related Manage Mandate(s)

Manage Mandate(s) Get Mini Statement

Get Mini Statement

categories

categories Bloggers

Bloggers Blog collection

Blog collection Press Release

Press Release

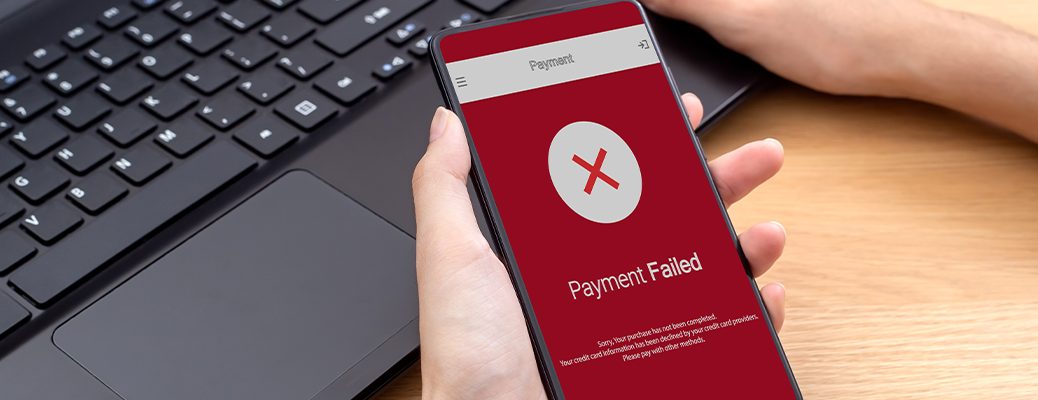

So, you spent a long day at work, dedicatedly earning every rupee. You finally come home and decide to reward yourself with an online purchase. Excitement fills you up as you enter your credit card details to finalise the purchase. But then, the unexpected happens. Your screen flashes a message: “Transaction Failed.” Confused, you quickly check your bank app, and it shows money debited. That feeling of stress is something natural in such situations.

But it’s not just the inconvenience that bothers you. It feels like your hard-earned money has just disappeared. And now you are left with so many questions and concerns. How do you react in such a situation? What steps should you take to make sure your money is safe? Let’s find out.

Credit Card Transaction Failed but Amount Debited? Steps to Take

Here are some actions you can take to address this issue and protect your finances.

- Verify the Debit First

Firstly, check if the money has been debited from your account. Open your credit card statement through online banking or a mobile app. Look for the specific transaction that failed. If you see the amount debited, note down the transaction details. These include the date, amount, and merchant name.

- Contact the Merchant

Upon finding that your credit card transaction failed but amount debited, your next action is to reach out to the merchant.

Use their customer support or help desk. Explain the situation to them. Try to provide all relevant details about the transaction, such as time, date, and amount debited. This will help the merchant check their records with more precision. If it turns out your initial transaction failed, but the payment still got debited due to a discrepancy, they may propose solutions, such as a refund or a repeat of the service.

- Document Everything

Keep a record of every step you take. Document all communications with the merchant and the bank. This includes emails, chat logs, and phone call records. Save copies of bank statements showing the debited transaction. Organise these documents chronologically. This organised documentation can be presented as proof if needed later.

- Dispute the Credit Card Transaction

If conversations with the merchant do not yield results, you can dispute the transaction. Contact your bank’s customer service and file a formal dispute claim. Offer all necessary evidence, such as transaction details and your communication records with the merchant. The bank will then investigate the matter to check the validity of your claim.

You can even visit a bank physically and talk to a representative there. When you speak with someone in person, it’s easier to explain complex situations, clarify specific details of the problem, and get immediate feedback. Also, you have the chance to ask multiple questions right away, which helps you understand the process more clearly and know what actions are exactly required.

- Follow Up from Time to Time

After you file a dispute, stay in touch with your bank. Track the progress of your credit card dispute and make inquiries. Routine follow-ups help ensure that your case does not get delayed or forgotten. Be persistent but also be patient. After all, banks often have specific timelines for resolving such issues. So, adjust your expectations accordingly.

Wrapping Up the Discussion on Failed Credit Card Transactions

Handling a failed credit card transaction where money has been debited can be a stressful experience. No one wants to see their hard-earned money stuck in a transaction error. However, with the correct steps and patience, you can address the problem efficiently. Just remember that such incidents, while inconvenient, are often resolvable with time and the right actions.

As a useful tip, you can choose an IndusInd Bank credit card to get 24/7 customer support to deal with any kind of banking issues. Their customer-centric approach and round-the-clock assistance mean that help is always just a call away. Moreover, the process to apply for an instant credit card is simple and 100% digital.

Apply for an IndusInd Bank credit card now and get instant approval.

Disclaimer: The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. Hence, you are advised to consult your financial advisor before making any financial decision. IndusInd Bank Limited (IBL) does not influence the views of the author in any way. IBL and the author shall not be responsible for any direct/indirect loss or liability incurred by the reader for taking any financial decisions based on the contents and information.